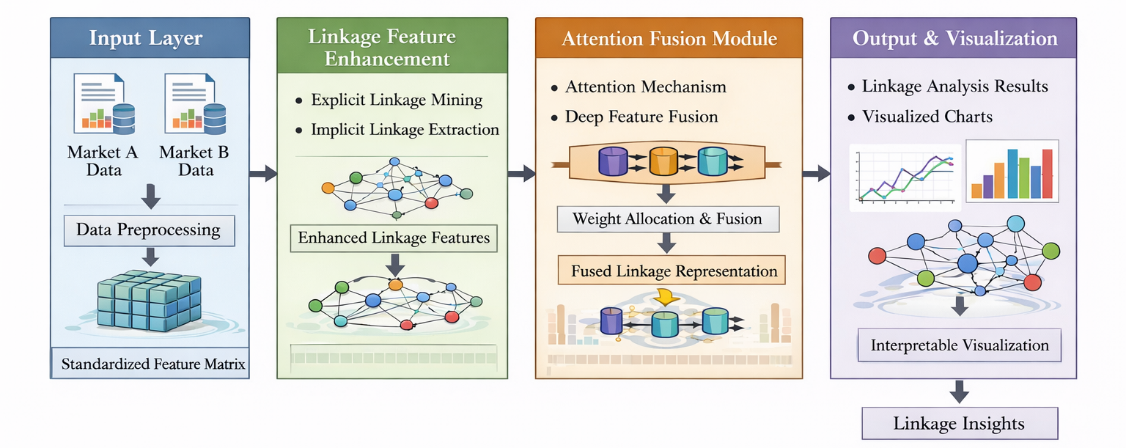

This paper selected monthly time series data from both markets from January 2018 to December 2023. Data preprocessing and feature design were performed, and several experiments were carried out with LSTM, CNN-LSTM and Transformer as models. MAE, RMSE and LCE, which can achieve a lower 0.023, 0.031 and 0.018, respectively, with R2 =0.942, are achieved by TLAEFNA. The prediction accuracy and linkage feature capture are much superior to mainstream time series models, and are stable and robust when the data is insufficient and outlier interference is present. By implementing a visualization module, our algorithm intuitively presents linkage trends, attention weights and factor importance, which reveal the temporal and regional differences in the linkage between the real and securities markets and identifies the principal linkage factors such as housing price changes, real estate stock transaction volumes and funds and expectations transmission paths. This algorithm solves the black-box problem of machine learning that provides accurate and interpretable technical support for cross-market investment decisions, risk warnings and policy regulation.