About AEMPSThe proceedings series Advances in Economics, Management and Political Sciences (AEMPS) is an international peer-reviewed open access series that publishes conference proceedings from a wide variety of methodological and disciplinary perspectives concerning economic and management issues. AEMPS is published irregularly. The series welcomes empirical and theoretical articles concerning micro, meso, and macro phenomena. Proceedings that are suitable for publication in the AEMPS cover domains on various perspectives of economics, management and political sciences and their impact on individuals, businesses and society. |

| Aims & scope of AEMPS are: · Economics · Management · Political Sciences |

Article processing charge

A one-time Article Processing Charge (APC) of 450 USD (US Dollars) applies to papers accepted after peer review. excluding taxes.

Open access policy

This is an open access journal which means that all content is freely available without charge to the user or his/her institution. (CC BY 4.0 license).

Your rights

These licenses afford authors copyright while enabling the public to reuse and adapt the content.

Peer-review process

Our blind and multi-reviewer process ensures that all articles are rigorously evaluated based on their intellectual merit and contribution to the field.

Editors View full editorial board

London, UK

canh.dang@kcl.ac.uk

Leeds, UK

S.Amini@lubs.leeds.ac.uk

Cardiff, UK

EshraghiA@cardiff.ac.uk

London, UK

alexandre.loktionov@kcl.ac.uk

Latest articles View all articles

The COVID-19 pandemic, geopolitical conflicts and extreme climate events have disrupted global supply chains, exposing the fragility of the traditional efficiency-first model. Taking political, economic risks and natural risks as research objects, this paper reviews risk identification theories and deconstructs two cases—Apple's friendshoring and Toyota's response to the Great East Japan Earthquake—to extract behavioral logic and decision-making mechanisms against different risks. The study finds that firms need to shift from passive emergency response to active defense, establishing a four-stage framework "Prediction–Protection–Buffering Recovery", with comprehensive implementation of strategies covering four dimensions: multi-sourcing, dynamic buffer inventory, digital monitoring and optimization of supply chain network structure. This paper points out that current research still lacks sufficient discussion on the interactive mechanism between enterprises' micro-level dynamic capabilities and risk management. Future research can further explore how emerging technologies reshape the practical paradigm of supply chain risk management. This study offers theoretical insights and practical implications for risk management decision-making in multinational corporations amid intensifying uncertainties in global supply chains.

The construction industry is characterized by long project cycles, substantial upfront capital requirements, slow cash inflows, and high cash flow volatility, making working capital management a critical factor affecting the survival and development of construction enterprises. This paper focuses on working capital management in the construction sector, systematically analyzing its fundamental concepts, industry-specific features, major challenges, and optimization strategies. Employing literature review and inductive analysis methods, the study delves into common issues such as delayed payments, inefficient accounts receivable and payable management, excessive capital tied up in inventory and work-in-progress and inaccurate financial forecasting. These challenges can be addressed through improved cash flow forecasting and monitoring, optimized accounts receivable and payable processes, enhanced inventory and supply chain coordination, and strengthened policy support. Research shows that the problems in the operational capital management of the construction industry are interrelated and mutually influential. To enhance the efficiency of operational capital, it requires the joint efforts of internal improvement within the enterprise and external cooperation.

In modern corporate finance, the weighted average cost of capital is an important indicator for evaluating financing decisions, investment projects and enterprise valuation. With changes in market interest rates, investor expectations and operating risks, enterprises need to understand how their capital structure affects the overall cost of capital. This study examines how capital structure affects weighted average cost of capital (WACC) and corporate valuation using Costco Wholesale Corporation as a case. Based on Costco's FY2024 financial data and market inputs around September 2024, the study estimates the cost of equity, after-tax cost of debt, and market value weights. The result shows that Costco's FY2024 WACC is 7.539%, WACC provides a practical framework for evaluating enterprise financing decisions and company valuation. The analysis of Costco Wholesale Corporation shows that maintaining a balance between debt and equity helps improve financing efficiency and supports long-term value creation. The findings in this paper suggest that Costco maintains a conservative capital structure and that WACC is useful for evaluating financing decisions and long-term firm value.

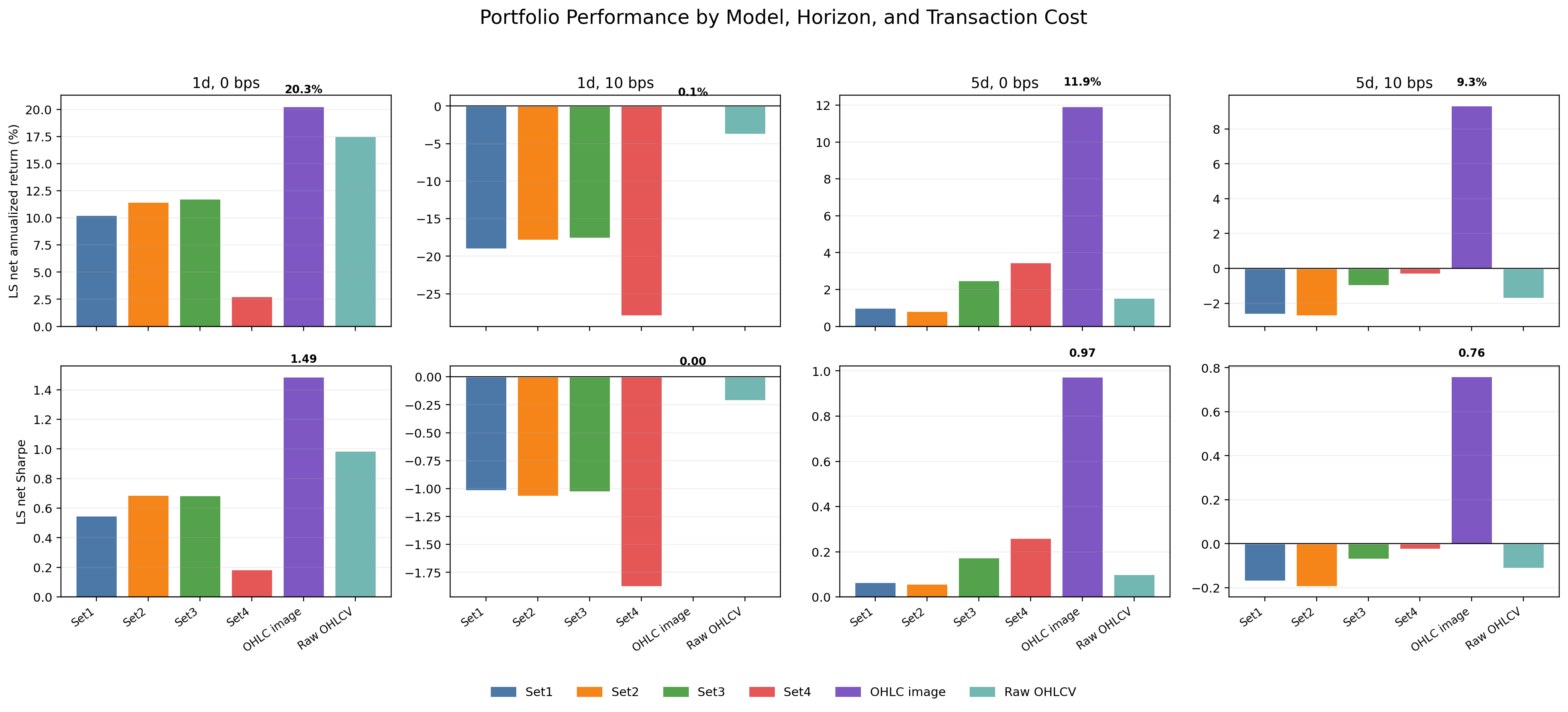

This paper examines whether technical information can generate economically meaningful stock portfolio returns under transaction cost constraints. Using daily data for CSI 300 constituent stocks from April 2, 2019, to December 30, 2025, this paper compare basic price-volume variables, traditional technical indicators, market-state variables, StockJump and VPIN microstructure variables, OHLC image CNN, and Raw OHLCV CNN models. Instead of relying mainly on classification metrics such as AUC and Accuracy, this paper evaluate models through out-of-sample quintile portfolios, focusing on long-short returns, Sharpe ratios, turnover, and transaction-cost-adjusted performance. The results show that traditional technical indicators, market-state variables, and microstructure variables provide limited incremental value beyond basic price-volume information. The 1-day prediction task exhibits some cross-sectional sorting ability, but its returns are largely eroded by high turnover after 10 bps transaction costs. In contrast, the 5-day OHLC image CNN retains a 9.34% long-short net annualized return and a 0.761 net Sharpe after costs, outperforming structured feature models and Raw OHLCV CNN. These findings suggest that technical information should be evaluated by portfolio-level economic value, and that image-based price-path representation better captures nonlinear information over longer horizons.

Volumes View all volumes

Volume 292August 2026

Find articlesProceedings of ICFTBA 2026 Symposium: Strategic Management & Business Analytics: Data-Driven Performance Models

Conference website: https://2026.icftba.org/London/Home.html

Conference date: 29 October 2026

ISBN: 978-1-80590-911-8(Print)/978-1-80590-912-5(Online)

Editor: An Nguyen

Volume 291August 2026

Find articlesProceedings of ICEMGD 2026 Symposium: The Role of Blue Economy in Promoting Human Sustainable Development

Conference website: https://2026.icemgd.org/Galati/Home.html

Conference date: 28 September 2026

ISBN: 978-1-80590-907-1(Print)/978-1-80590-908-8(Online)

Editor: Florian Marcel Nuţă

Volume 290August 2026

Find articlesProceedings of the 10th International Conference on Economic Management and Green Development

Conference website: https://2026.icemgd.org/

Conference date: 28 September 2026

ISBN: 978-1-80590-889-0(Print)/978-1-80590-890-6(Online)

Editor: Florian Marcel Nuţă

Volume 289July 2026

Find articlesProceedings of ICEMGD 2026 Symposium: Rethinking Governance and Policy Innovation for Societal Challenges

Conference website: https://2026.icemgd.org/Lahore/Home.html

Conference date: 7 July 2026

ISBN: 978-1-80590-893-7(Print)/978-1-80590-894-4(Online)

Editor: Ahsan Ali Ashraf , Florian Marcel Nuţă

Announcements View all announcements

Advances in Economics, Management and Political Sciences

We pledge to our journal community:

We're committed: we put diversity and inclusion at the heart of our activities...

Advances in Economics, Management and Political Sciences

The statements, opinions and data contained in the journal Advances in Economics, Management and Political Sciences (AEMPS) are solely those of the individual authors and contributors...

Indexing

The published articles will be submitted to following databases below: