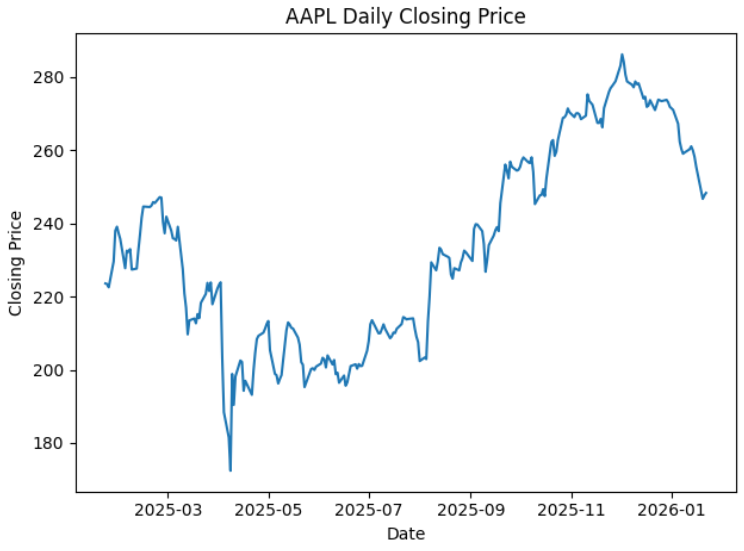

Stock return prediction is a fundamental but difficult issue in financial research because of the noise and dynamics of market data. Although recent research has improved the ability of existing machine learning model prediction, these methods are difficult to interpret and lack practical application value due to their "black box" nature. This paper constructs an explainable machine learning framework to achieve high-accuracy predictions of short-term stock excess returns and strive for greater interpretability in economics; Compared with other complex models. Taking the daily trading data of Apple Inc. (AAPL) as a single-stock example, this paper constructs a set of economically meaningful features based on historical returns, volatility and trading volume. A linear regression model is used as the central prediction tool, and interpretability can be built into this specific form of a linear model. Out-of-sample forecasts use the rolling window method, and prediction performance is compared with a naive historical mean benchmark. Based on experiments, the current basis of explanation using an explainable linear model has been shown to be relatively stable in baseline prediction. According to the coefficient analysis, in addition to conforming to some basic Finance theory patterns. A return pattern that exists for one day appears. A Volatility-Return relationship also holds currently. This paper shows that interpretive models, in combination with carefully selected features, achieve satisfactory prediction performance; at the same time, it is also found through the analysis of economic implications that such an approach helps explore the essence of changes in stock returns.