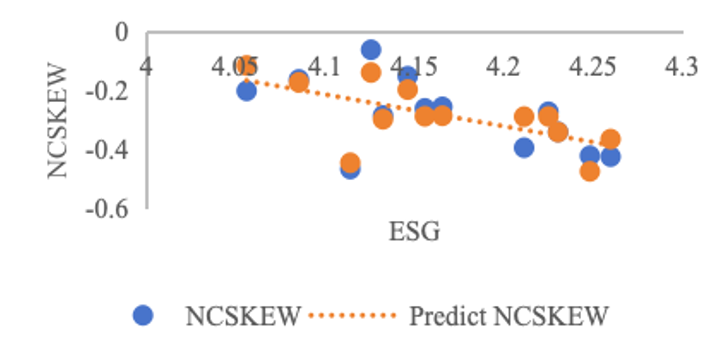

This study analyzes how the disclosure of ESG ratings influences the possibility of stock price crashes in the Chinese stock market, by employing a quantitative research methodology, utilizing a large sample of data on ESG ratings, stock prices, and other relevant financial metrics of Chinese companies for the period 2009-2022 from the CRSP and Hexun website. The results reveal that higher ESG ratings are linked to lower information asymmetry between firms and the market, leading to a reduced risk of stock price crashes. Through regression analyses, it is worth noting that while ESG scores generally correlate with decreased crash risk, the impact varies across different sectors, with traditional industries showing less sensitivity to ESG ratings. This suggests a critical need for enhanced promotion and enforcement of ESG practices within the Chinese market. Overall, this research contributes to the growing body of literature on sustainable finance and offers practical insights into the significance of ESG criteria in the context of emerging markets.