Research Article

Open Access

Published 20 July 2025

DOI: 10.54254/2754-1169/2025.25278

Enhancing Stock Price Prediction Through Sentiment Analysis A FinBERT-LSTM Approach to Market Sentiment Integration

Yunjie Chen, Junjie Liu, Peize Gao

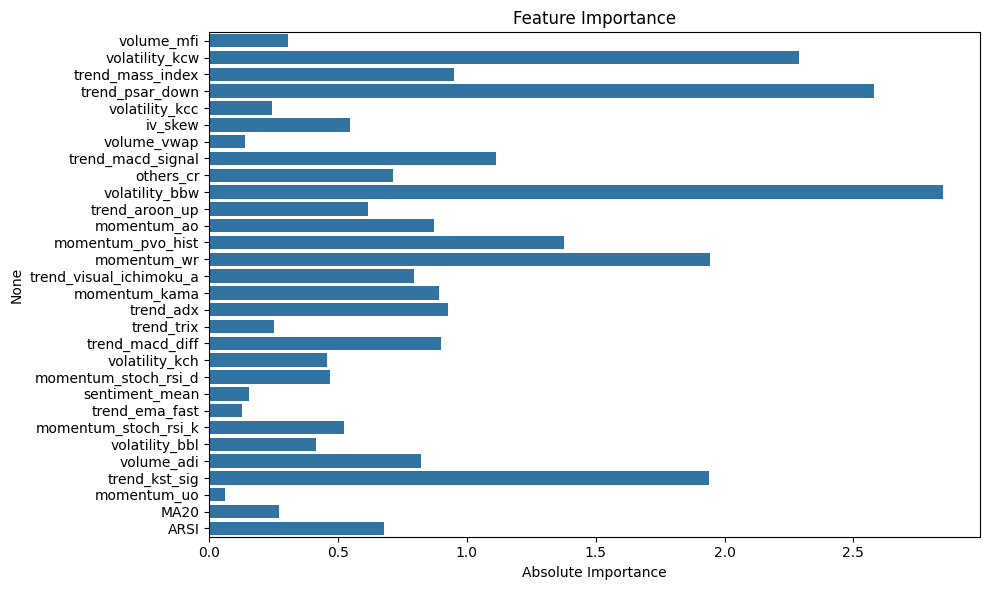

Stock price prediction remains a complex challenge in financial markets due to the dynamic interplay of economic indicators, global events, and investor sentiment. This study explores the integration of sentiment analysis into stock price forecasting using a FinBERT-LSTM model. By leveraging financial news data and market indicators, we aimed to enhance predictive accuracy. Sentiment features, such as sentiment intensity and daily sentiment ratios, were extracted using the FinBERT model and combined with traditional market data in an LSTM framework. Comparative analysis demonstrated that the sentiment-enhanced model significantly outperformed the baseline LSTM model, particularly during periods of high market volatility. These findings highlight the critical role of sentiment in market dynamics, providing a foundation for more robust predictive models. Future research directions include the incorporation of additional sentiment sources and advanced model architectures to further improve performance and adaptability in diverse market conditions.

Research Article

Open Access

Published 3 September 2025

DOI: 10.54254/2754-1169/2025.26444

The Impact of Capital Market Opening on the A/H Premium: From the Perspective of ETF Connect

Zihan Zuo, Boshen Chen, Qiyao Zhou

Seng China A/H Premium Index, taking into account variables measuring exchange rate, market sentiment, and the A/H risk-free spread. The empirical results show that the ETF Connect initially increased the A/H premium, due to market adjustment and external factors like the Federal rate hikes. With several subsequent expansions as well as improvement, the ETF Connect then significantly reduced the premium, suggesting improved market efficiency and integration. In this work, we conclude that ETF Connect has the potential to further narrow the A/H share premium, especially in the post-pandemic and rate-cutting environment, thereby promoting value investing in the A-share market. This study contributes to the literature by providing a macro perspective on the correlation between the ETF Connect and the A/H premium, highlighting the importance of capital market integration in reducing price discrepancies and fostering a more efficient investment landscape.

Research Article

Open Access

Published 3 September 2025

DOI: 10.54254/2754-1169/2025.26453

The Impact of ESG Scores on the Corporate Financial Performance of China’s Listed New Energy Companies

Siqi Zhang, Zhangyu Sima, Han Ma, Wenxuan Zhu, Yiling Zhuo

When looking at the impact of ESG scores on energy companies’ financial performance, we found that a company's ESG performance significantly affects its financial performance. A high ESG score often reflects stronger risk management, lower capital cost, and higher investor trust. This positive relationship is likely to reinforce profitability and competitiveness of energy companies in the market in the long run, with increasingly severe environmental regulations and greater awareness of social responsibility. Through an in-depth analysis of the above impacts. In other words, we are in a better position to understand how companies may improve their financial stability along with sustainability potential by optimizing their ESG performance.

Research Article

Open Access

Published 9 September 2025

DOI: 10.54254/2754-1169/2025.26650

Does Environmental Policy Stringency Affect the Productivity of the Industrial Sector in China? An Empirical Analysis of the Porter Hypothesis

Chujun Xu

This paper focuses on the effects of environmental policy stringency (EPS) on the total factor productivity (TFP) growth of firms, which is an extension of the Porter Hypothesis (PH). PH states that strict environmental regulations can promote enterprise innovation and improve enterprise productivity. To test this, the paper uses the word frequency of the keyword in the government report of China from 2010-2020 to test the EPS and chooses the TFP of firms from 2010-2020 as the indicator of the change in productivity of enterprises. The paper also uses panel data methods and ordinary least squares to test the relationship between EPS and TFP. In terms of policies, the national government should consider the economic gap between different regions and the different pollution levels between different companies.

Research Article

Open Access

Published 9 September 2025

DOI: 10.54254/2754-1169/2025.26715

Under the Presence of Digital Platforms, What Are the Gender Factors That Influence Consumers When They Purchase Secondhand Goods?

Zihan Zhou, Jiaran Zhang, Miao Miu, Yitong Sun

This study explores gender factors that influence consumer behavior in the secondhand goods market on digital platforms. In the context of growing ecological awareness and circular economy, understanding these factors is essential to optimize online sales strategies. The study identifies five key factors: price sensitivity, trust in digital platforms, environmental awareness, the impact of social networks, and consumer utility. The results indicate that women tend to be more price-sensitive than men, have more confidence in digital platforms, and are more environmentally conscious. The messages underscore the importance of targeted marketing and designing platforms that meet gender-specific preferences, thus improving the efficiency of the secondhand goods market. By focusing on the intersection of gender dynamics and online secondhand shopping, this study fills a gap in the existing literature and provides valuable information for e-commerce businesses and sustainability advocates.

Research Article

Open Access

Published 22 October 2025

DOI: 10.54254/2754-1169/2025.28371

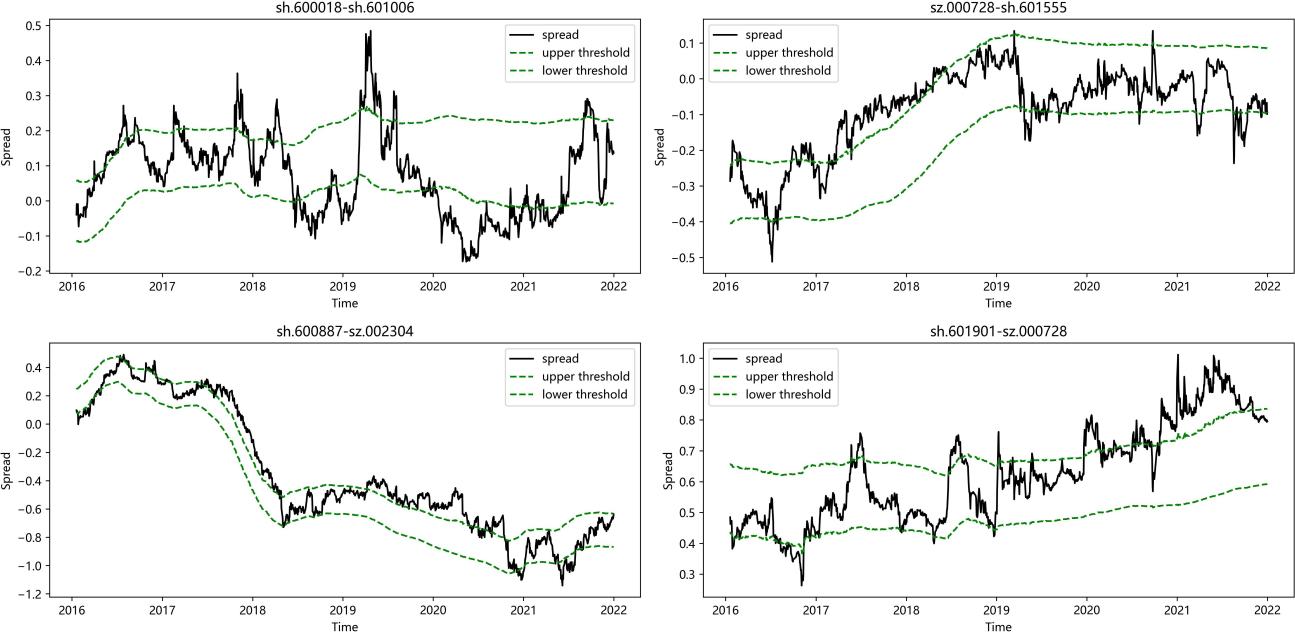

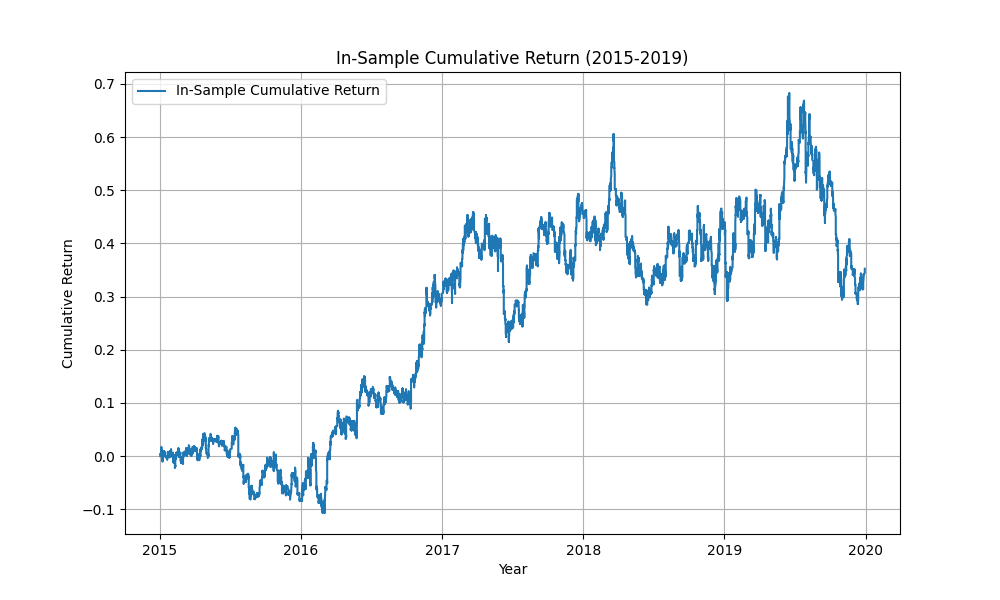

Statistical Arbitrage with Pairs Trading: Empirical Analysis in Chinese Market

Ouyang Feixue, Yanchen Liu, Zhenshan Zhang, Qizheng Yang

Our analysis of statistical arbitrage is based on the assumption that the spread of two assets follows a mean-reversing Ornstein–Uhlenbeck process when two assets are paired. By incorporating the cointegration test, Hurst component, and optimization into this framework, we develop a technique to identify the best pair in the market and verify the profitability of the pair trading strategy in China’s A-share Market. Although individual pairs may exhibit periods of inconsistency, constructing a diversified portfolio of multiple pairs significantly enhances performance.

Research Article

Open Access

Published 22 October 2025

DOI: 10.54254/2754-1169/2025.28381

How Markov Chain and Fama-French Be Used in Practical Financial Alpha Strategy

Ruijie Mao, Xinxing Li, Jiaxuan Li, Yang Yang, Siyuan Fan

According to Tulchinsky, Igor, et al’s Finding Alphas: A Quantitative Approach to Building Trading Strategies, the model that predicts the price of a financial instrument is called alpha. This paper presents two alpha strategies based on the Markov chain model. which predicts future stock price movements by analyzing the transition probabilities between different market states and the Fama-French model, in which market performance. Note that the general possibility of the Market trend, which is the alpha of the Markov Chain is by using variables: price changes, sentiment, and trading volume. This is a commonly used market prediction method; however, innovation can be made in the interpretation of this possibility. The strategy uses historical data from 2015 to 2023 to create market-neutral short- and long-term portfolios. and we make sure the monetary neutrality to give a general and consistent performance of our alpha strategy.

Research Article

Open Access

Published 6 November 2025

DOI: 10.54254/2754-1169/2025.28885

Example Business Models of Electric Vehicle Startups in China and the US

Yijun Liao, Zidong Mo, Yuan Gao

In the modern era, electric vehicles are developing at a rapid speed, and technology and sales have made breakthroughs. Among them, in recent years, many mature brands have been established in the electric vehicle markets of China and the United States, such as Tesla in the United States and BYD in China, and many new brands have emerged. This article mainly studies the political, economic, social, technological, environmental and legal differences between the China and the United States in the development of electric vehicles, and conducts a detailed market analysis of a single brand to better understand the development of electric vehicles.

Research Article

Open Access

Published 6 November 2025

DOI: 10.54254/2754-1169/2025.28879

Exploring the Redundancy and Novelty in Factor Discovery: A Literature Review on Correlations Between Investment Factors

Hao Yin, Yuehua Wang, Ziyuan Wang

Often referred to as the "factor zoo," the fast spread of investment variables has sparked intense discussion about the true uniqueness of many recently discovered variables. With an eye toward the correlations that can compromise their uniqueness, this literature review investigates the degree to which these elements simply restate information already obtained by other elements. The consequences of these correlations for portfolio building, diversification techniques, and risk management are investigated in this review. It uses important research, including the significant work by Feng et al., in order to give a whole picture of the redundancy and value of investment variables. The results provide insights on improving factor-based investment strategies by stressing the difficulties in differentiating between really unique elements and those that repeat existing knowledge.

Research Article

Open Access

Published 6 November 2025

DOI: 10.54254/2754-1169/2025.29011

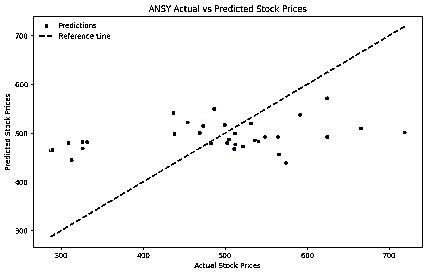

Impacts of Climate Factors on UK Insurance Companies: Evidence from the Stock Prices

Yuqing Qian, Zhongchi Wang, Fan Ye

Climate change poses significant risks to the insurance industry, particularly through increased frequency and severity of weather events. In this paper, we examine the extent to which temperature, wind speed, and rainfall influence the stock prices of companies listed on the UK stock market. By using data of 1. Andrews Sykes Group plc. (ANSY) 2. Aviva plc (AVIVA) 3. Legal & General Group plc (LGEN) 4. Prudential plc (PRU) 5. Direct Line Insurance Group plc (DLGD) and conducting the multiple linear regression model and random forest model, the findings, illustrated through scatterplots, indicate a weak relationship and correlation between the dependent (stock prices) and independent variables (weather data), as shown by the P-values and R-values.