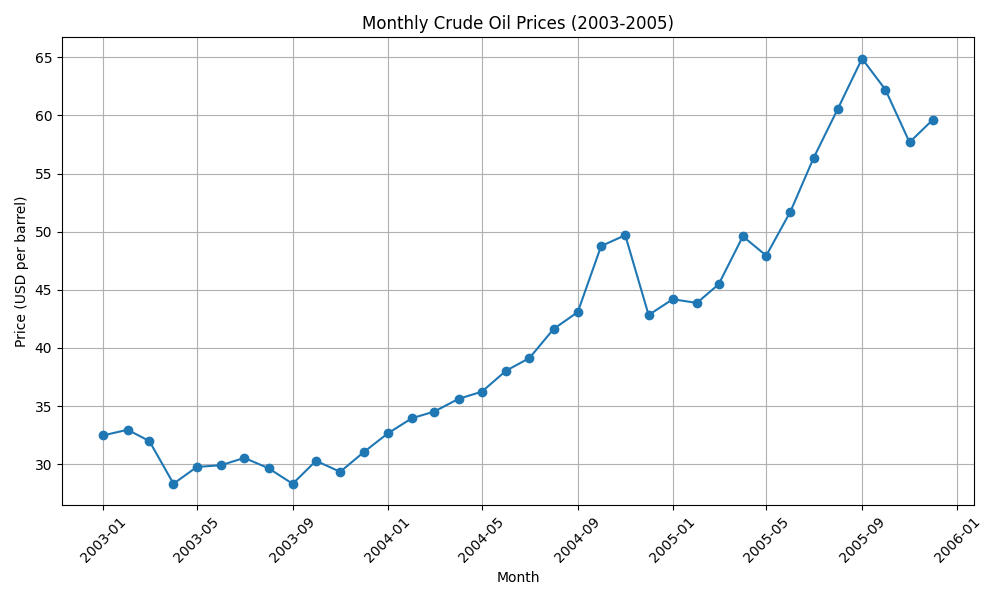

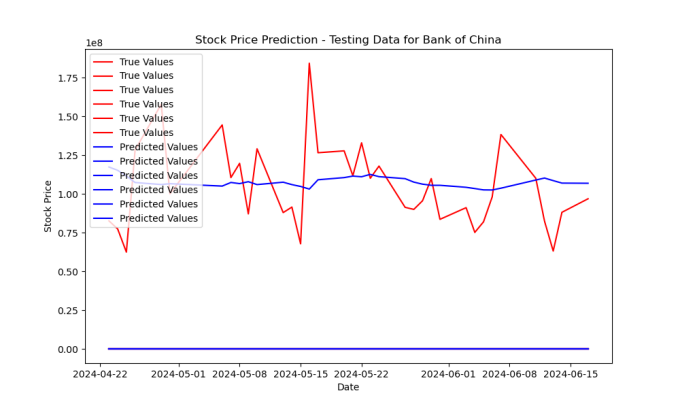

Stock price prediction in the volatile and evolving China A-share market faces both a challenge and an opportunity. In this paper, an attempt is going to be made to implement Long Short-Term Memory (LSTM) neural networks in predicting stock price movements of several large banks in China. The database comprises daily information on stocks of eight banks, split into training and testing sets. Development and Optimization of an LSTM Model Using MSE and the Adam Optimizer. The model exhibited quite good predictive capability over the training data but weak generalization over the unseen data. However, the study found that LSTM-based predictions could support profitable trading strategies, thus providing valuable insight for investors and policymakers. This could be further investigated by enhancing the robustness of the model and deploying across different markets and time frames.