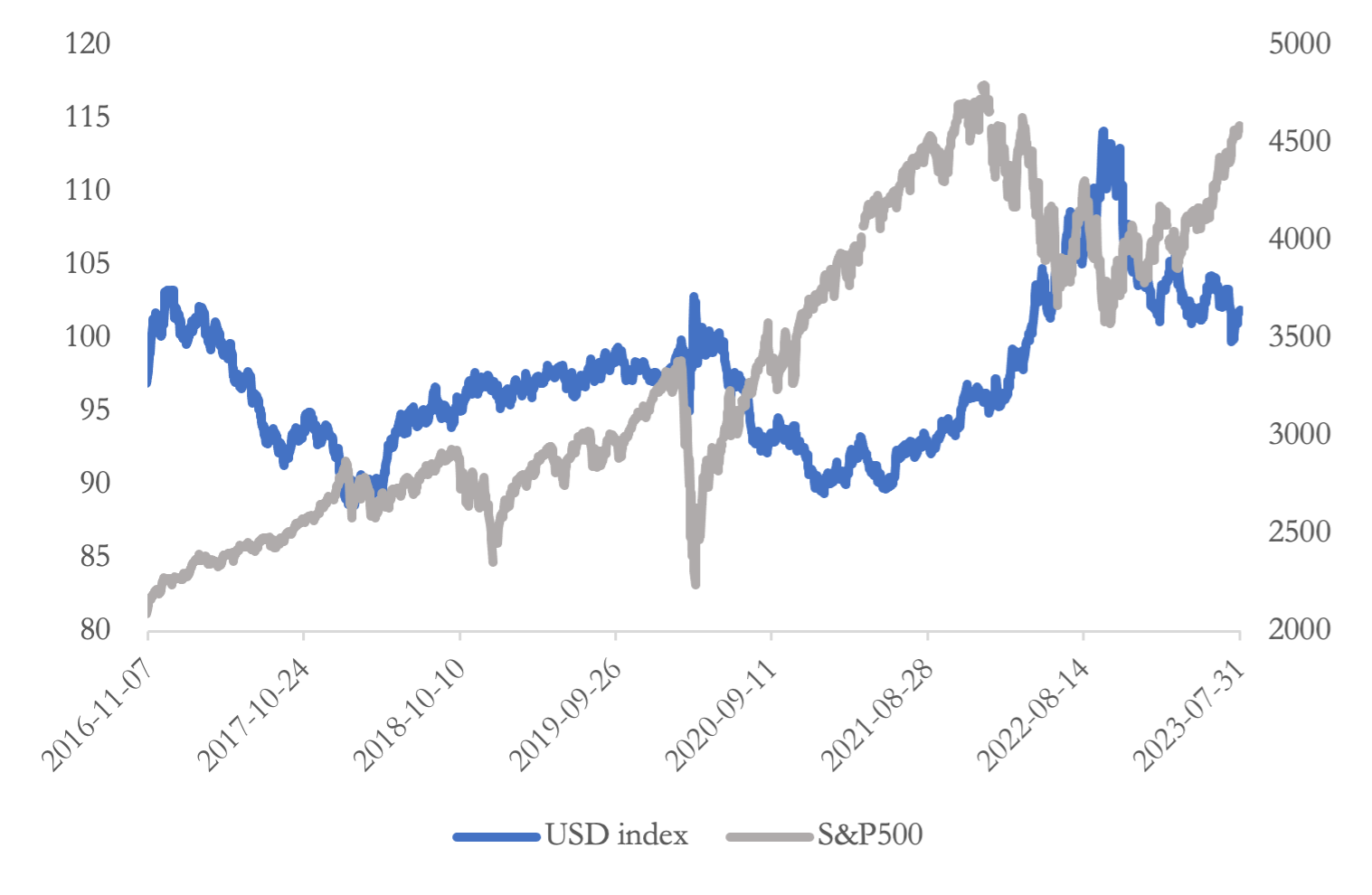

This paper investigates existence of equilibrium relationships among the USD index and S&P500 in the long term in the United States. By applying correlation matrix analysis to daily data for the 2016:07:30–2023:08:01 period, this paper finds that there was a slight negative correlation between the USD index and the S&P 500. Basing on the Augmented Dickey-Fuller test (ADF test), this paper shows that that the correlation between the USD index and the S&P 500 is stable while vector autoregressive model (VAR model) proving that changes in the USD index can cause changes in the S&P 500 index. Firstly, using ADF test and VAR model to investigate the relationships between the USD index and A&P500, this paper reveals not only judge the negative relationship between this two, but also studying the stability of this relationship, proving the validity to explain the changes of S&P500 by the changes of the USD index. This conclusion can act as a good judging basic for US leaders to make economic decisions such as raising or lowering interest rates.