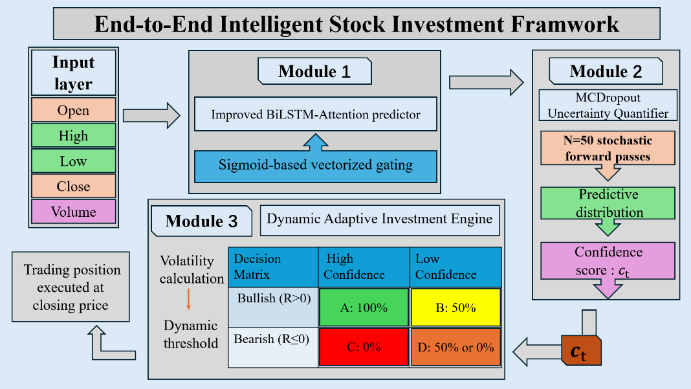

Regarding the lack of uncertainty quantification and the threshold rigidity in predictions of deep learning models, this paper proposes an intelligent investment framework based on an improved Bidirectional Long Short-Term Memory (BILSTM)-Attention model. The model chooses Sigmoid gating instead of Softmax attention to achieve non-competitive information aggregation. It also uses Monte Carlo Dropout by performing multiple random forward passes during the prediction phase and estimates the uncertainty of the predictive distribution, which is mapped to confidence. Based on this, the paper designs a dynamic threshold mechanism, adjusting the threshold according to market volatility and generating a 'prediction & confidence' signal to guide portfolio rebalancing. The experiments on three A-share semiconductor stocks show that the improved model generally outperforms the standard Long Short-Term Memory (LSTM) and the baseline BILSTM-Attention model. The backtesting shows that after introducing the confidence, the strategy's total return increased from 3.64% to 5.12%, and the maximum drawdown decreased; the dynamic threshold further increased the return and Sharpe ratio to 5.97% and 2.17. The framework of this paper improves prediction accuracy and investment performance, providing new ideas for quantitative investment.