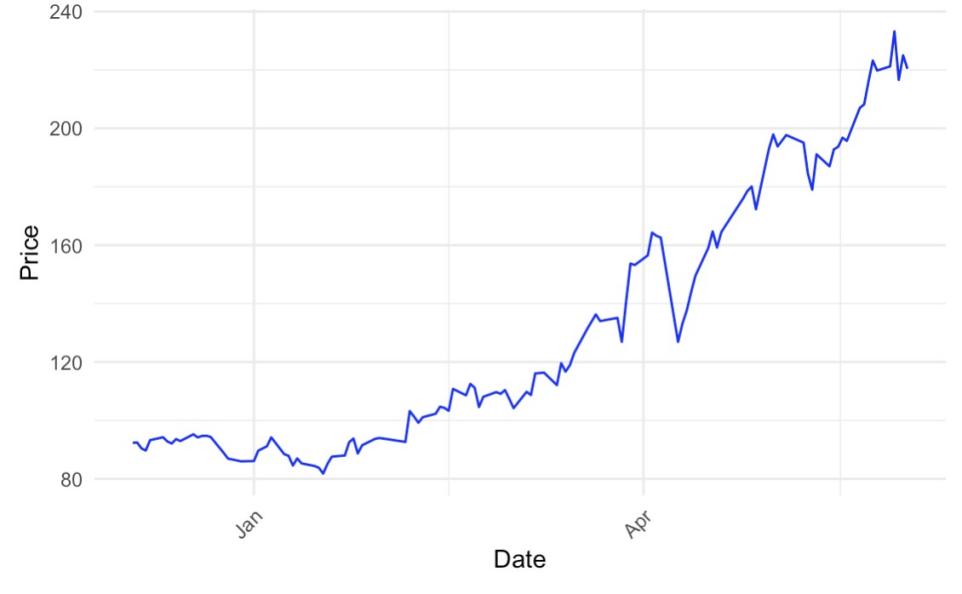

With the increasing sophistication of financial management techniques, the ability to predict stock prices has become a critical endeavor for investors and traders. The Autoregressive Integrated Moving Average (ARIMA) model stands out as a widely used method for forecasting stock price movements. This model, which belongs to the class of time series analysis, is particularly adept at estimating daily returns with associated confidence intervals. The present study aims to apply the ARIMA model to forecast the share prices of Pop Mart. The dataset encompasses the period from December 2024 to May 2025, focusing on the opening prices as key variables. The analysis reveals that the ARIMA model is capable of capturing the fluctuations in stock prices with a certain degree of accuracy. The Mean Absolute Percentage Error (MAPE) value of 6.86%, which is significantly below 10%, suggests that the predictive performance is commendable. Furthermore, the insights gleaned from this model offer investors and traders valuable guidance for interpreting market trends and assessing potential risks, thereby enhancing their decision-making capabilities.