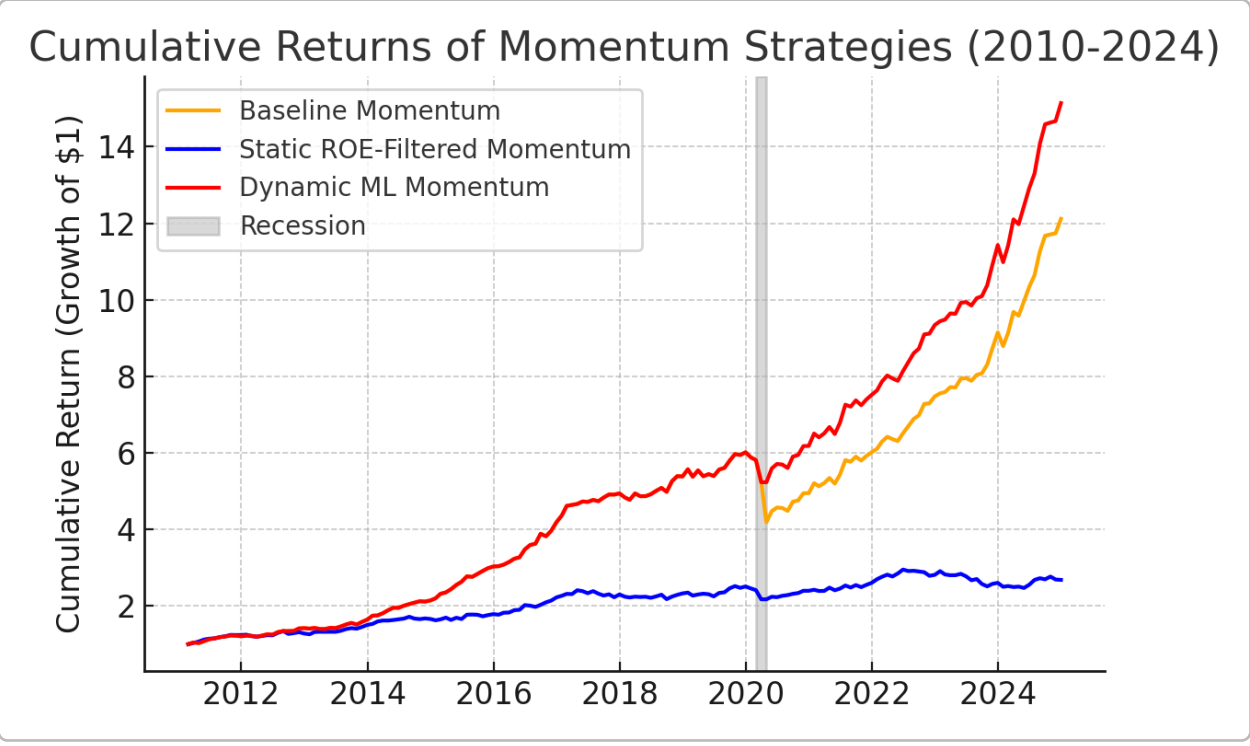

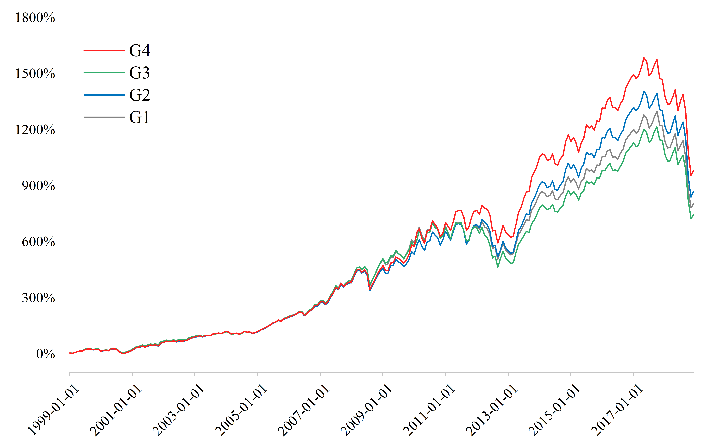

Constructing risk control strategies that are adaptive to market movements is an important trend in portfolio selection. In the existing literature, constructing a tail risk control model based on conditional value-at-risk (CVaR) has been widely used. Traditional literature is based on a singleβlevel for risk control, However, the portfolio effect is highly sensitive to theβlevel, which makes it difficult to output stable and reliable strategies. In addition, there have been studies examining the control of tail risk under multipleβklevels at the same time for differentβkits risk threshold is set the same. However, this uniform threshold makes it difficult to differentiate the responsiveness to the market. Accordingly, this study introduces the CVaR in multiple confidence levels of the differentiated thresholds so that the strategy has a more elastic risk control ability. In addition, the fixed threshold setting is easy to use in the highly variable market environment to show the limitations. Accordingly, this study constructs a linearly scaled dynamically adjusted portfolio strategy based on the market Chicago Board Options Exchange Volatility Index (VIX), As a result, it is found that the strategy has good adaptability with high risk-adjusted returns on different types of asset datasets. This suggests that the strategy provides the responsiveness of traditional CvaR strategies to tail risk and structural adaptation to market movements.