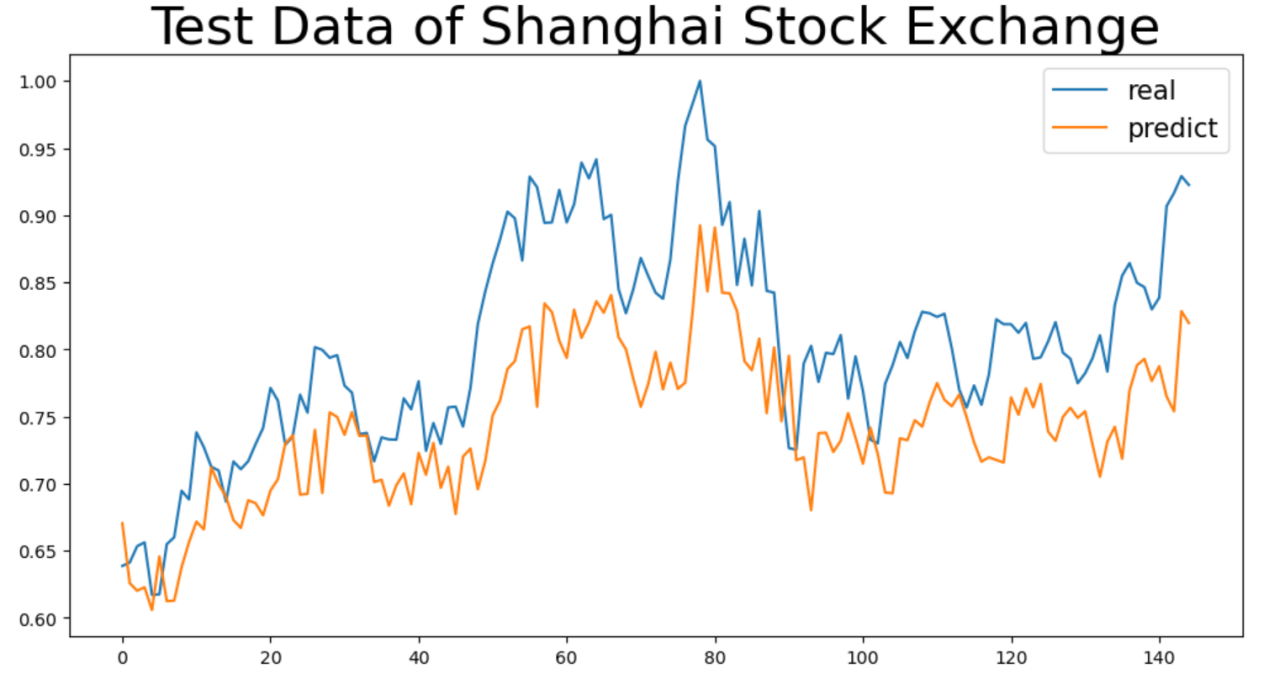

Stock price prediction faces significant challenges due to the high complexity and non-linear characteristics of financial markets. Traditional models often struggle to effectively capture their dynamic patterns. This paper, based on the Backpropagation Neural Network (BPNN), constructs a multivariate time series forecasting model to explore the non-linear mapping relationship between historical trading data, such as opening price, closing price, lowest price, and highest price, and the next day’s closing price. To demonstrate the practical applicability of the model and the impact of data time span, two comparative experiments were designed, using two years and three years of historical data, respectively, to analyze stock price predictions for 13 major global securities markets. Empirical results show that BPNN exhibits strong forecasting ability in stable markets. Extending the time span can improve the prediction accuracy for some markets by covering a more complete market cycle. However, the effect is constrained by market volatility and external environmental factors. The research findings provide a theoretical basis for cross-market model adaptation and data governance strategies.