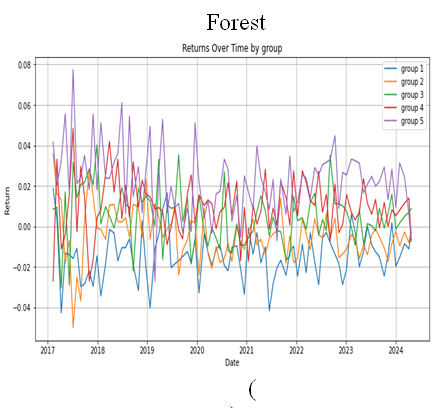

This paper takes 23 features of China's actively managed funds from 2015 to 2024 as samples, and predicts the future returns of the funds based on traditional linear regression models, Elastic Net models, Decision Tree models, Random Forest models, Ridge Regression models and Lasso Regression models, and constructs investment portfolios in groups according to the predicted return. The effectiveness of the investment portfolio construction is examined by analyzing the Sharpe ratio, information ratio, volatility and maximum drawdown rate of real data, and the predictive ability and stability of the features are examined by analyzing the value of Rank IC and ICIR of the features. The study found that the features used in this paper can provide rich information for the model, and most of the features have strong predictive ability and predictive stability; the performance of each investment portfolio is consistent with the real data; compared with the traditional linear model, the machine learning method has higher prediction accuracy, more flexibility and stability.